HOUSING MATTERS

Things You Should Know About BTO VS Resale: Part 2

This article is a continuation of Things You Should Know About BTO vs Resale Part 1.

Just to recap, we have compared the financial aspect between buying a BTO compared to a resale. BTO won in terms of which will cost less money.

In this article, we will continue to compare these 2 options from another angle.

Everyone talks about buying a house but how about selling it? And how much of you CPFOA can you use to finance your flat? Let’s find out the answers.

Selling your house

After a few years, would you want to move house? Most couples would want to upgrade to larger flat or even get a private property. Well buying another house won’t be much of an issue unless you don’t have the finances.

But what about your current house? Are you able to sell it? Is there anyone that is interested in purchasing your flat? Will you be able to make a profit? Remember this, you are not allowed to own 2 HDB houses hence you do have to sell one off.

![]()

Most of you will understand that you have to pay back to your CPF Ordinary Account prior to getting the profit in cash. You do have to pay the loan balance, the amount that you have used for the loan, the interest from the loan and also the accrued interest. Yes, you have to pay back that much to your CPFOA.

You do not need to worry if you are not able to pay back all of the above back. You do not need to top up with cash. But at the same time, that basically means that you are selling at a loss or with no profit. That is just not logical, as most people have the intention of selling and making a profit.

Hence selling a resale might be a challenge for you, as you would have quoted a high selling price and making potential buyers stray away from that kind of price range. Unless your flat is really in high demand and that makes you on the upper hand.

For a BTO, it might be easier as the price is cheaper compared to a resale thus you do not have to sell it at a high price, making it a more of an attractive option towards potential buyers.

Then again, these are all perspectives and are examples from people. It might differ when it comes to your own situation

The limitation of using your CPF Ordinary Account

You are able to fully finance the purchase of your BTO via CPFOA. There is no limitation on how much you are able to use. Which is good news actually as you do not have to fork out cash in financing your property.

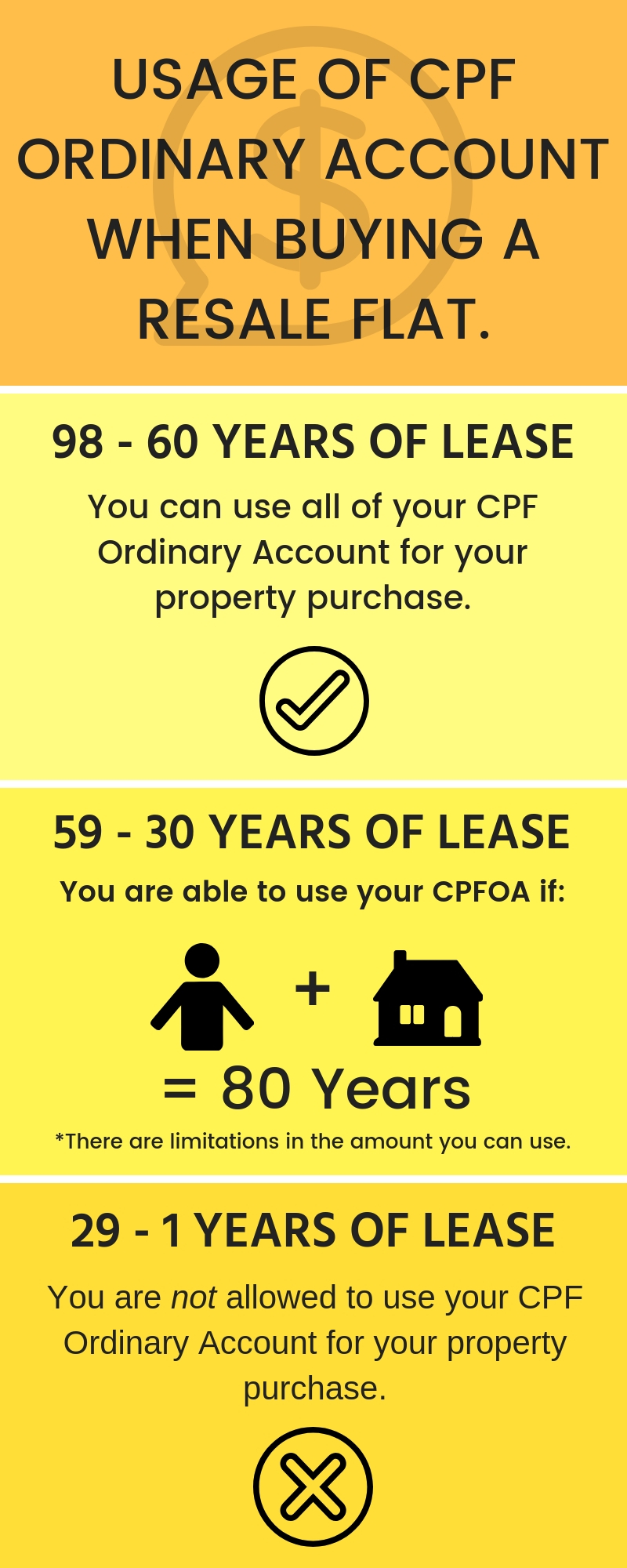

A different set of rules applies if you want to buy a resale. Depending on the remaining lease, there might be a limitation on how much of you CPFOA you are able to utilize in financing your resale flat. Refer to the graphic below.

For a resale flat with a remaining lease of 60 years and above, you can use all of your CPFOA for the purchase of your house. And at the other end, for resale flat with a remaining lease of fewer than 30 years, you are NOT able to use any of your CPFOA.

The real question is what is the limitation in using my CPFOA when purchasing a resale flat with a remaining lease of 30 to 59 years. Yes, you can use your CPFOA but there is a certain extent when you are not able to use your CPFOA and have to pay the remainder of your loan with cash.

Let’s find out the amount that can be used from CPFOA. You have to first establish the valuation limit of the flat.

Valuation Limit:

It is the lower of the purchase price of the flat OR the value of the flat.

You will then have to follow this formula:

With the amount that you have, that will the amount of CPF you can use to purchase your resale flat.

Let’s see this example:

Price of flat: $400,000

Market value of flat: $420,000

Age of Husband: 28 years old

Age of Wife: 26 years old

Remaining lease of flat: 55 years

- Youngest eligible owner (26) is the wife and the remaining lease of the house when she turns 55 years old is 26 years.

- Once again, the valuation limit is the lower of the purchase price or the valuation of the flat at the time of the purchase.

- In this example, the valuation limit will be the Purchase price of the flat which is $400,000

The result will be that you can only use $189,091 from your CPF OA in order to finance your resale flat. That is about 47% of the purchase price, which means that you have to finance the other 53% via cash. Unless you really and really want to purchase that place for a valid reason, you should not go ahead with the purchase.

Eventually, after 55 years, the lease will end and you have to vacate the house. And that is not an option you want to take if you have indeed put in cash worth 57% of the property. It might even be more if you are taking a loan due to any interest payable.

![]()

It is still totally up to you but do think long-term

Buying a resale definitely has its benefits and limitations. Nevertheless, I have seen people still purchasing it due to their own personal reasons. And buying a BTO does have the same amount of dilemma as well.

Nonetheless, it is not wrong to go for either option but I would suggest that you have to think long term when buying your house. List out the pros and cons, calculate and then decide.

Hope this article was useful. Do share with your family and friends. Till next time.

Disclaimer:

I am a financial adviser but I am not your financial adviser. Therefore, what is posted on this website, are my opinions and NOT to be taken as financial advice. Information provided might be relevant at this period of time but may be irrelevant due to alterations to rules, regulations or policies. The information provided is true to the best of my knowledge, but there maybe omissions, errors or mistakes.